Boris, Brexit and the bail out blues

- Accrue Staff

- Jul 31, 2019

- 6 min read

The new Prime Minister of the United Kingdom (UK) – its third in four years – has promised to take the country out of the European Union (EU) by 31 October. No ifs, no buts. Exactly how the colourful but controversial Boris Johnson aims to achieve in 99 days what his predecessor, Theresa May, failed to do in two years remains to be seen. The ruling Conservative Party remains divided and the risk of a no-deal Brexit (i.e. crashing out of the EU without a transition agreement to ensure seamless trade in goods and services) remains high.

The EU is unlikely to substantially revise the deal it offered May, and Johnson seems determined to leave, come hell or high water. The third alternative is simply to kick the can down the road and postpone the deadline, but this will also extend the uncertainty that has damaged business confidence on both sides of the Channel.

Further complicating things is that the UK Parliament has previously voted to block a no-deal Brexit scenario, and it has the final say in terms of the UK constitutional order. But it also failed to reach a majority on any other Brexit-related proposal, including the draft deals May negotiated with the EU. So what happens now is anyone’s guess.

NEIGHBOURLY MATTERS Even in this age of instant global communications, trade is heavily influenced by geography. Countries trade with their neighbours; South Africa exports more to Namibia than to the Netherlands. It is no surprise that 40% of the UK’s trade is with the EU. Eventually, whatever the outcome, business will adapt and trade will continue between these two neighbours. But in the meantime, a no-deal Brexit could cause enormous chaos, as thousands of containers moving over the Channel might be subject to customs clearance.

Further complicating things is the fact that in the globalised economy, much of what is traded is in the form of intermediate goods or inputs (i.e. chassis, wheels, engine components), not finished goods (i.e. cars). Sometimes, the same component crosses a border a few times in the process of manufacturing the final item. This means supply chains in the UK and the Continent face disruption. This comes as manufacturing is already struggling. July’s Markit Eurozone Manufacturing Purchasing Managers’ Index slumped to a six-year low of 46.4. The UK’s June Manufacturing Purchasing Managers’ Index was also at the lowest level since 2013.

Services – particularly banking, insurance and legal – are very important to the UK economy, and the City of London specifically. It is here where the shifts might be permanent, and already many global banks are setting up offices on the Continent to have a physical presence in the EU.

INVESTMENT PLUNGE While the UK economy has not entered a recession since the June 2016 referendum, and the economy overall has performed reasonably well, there are clear signs of stress. While overall gross domestic product growth last saw a negative quarter in late 2012, fixed investment spending by business has contracted six out of the past 10 quarters.

When there is uncertainty, businesses don’t invest. Sound familiar? Domestic fixed investment by South Af rican businesses contracted 11 out of the past 20 quarters. South Af rican businesses have instead invested abroad, with less than spectacular results. Sasol might be the poster child for this, but it is by no means alone. It wrote off R18 billion last week, largely related to its yet-to-be-completed giant US chemical plant. Like Eskom’s Medupi and Kusile power stations, this megaproject is significantly behind schedule and over budget (though it is private shareholders and not taxpayers who are on the hook).

Given the many financial links between South Africa and the UK, it is interesting to reflect on the performance of British assets in this environment.

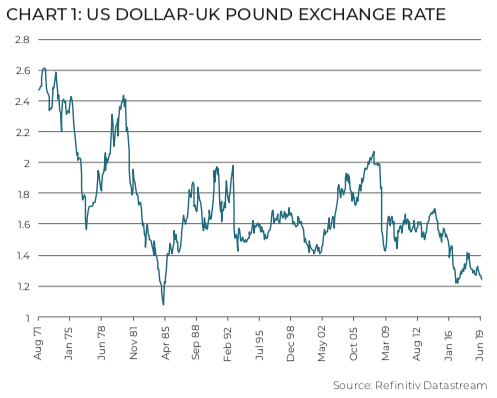

POUNDED The pound reflects all this uncertainty, jumping higher on any suggestion that there will be some sort of agreement (a ‘soft’ Brexit) and falling on indications of a no-deal (‘hard’) exit. It remains close to 34-year lows against the US dollar. The pound even fell 20% against the rand since the referendum. The weak pound, and the risk of further declines pushing up inflation means the Bank of England is unlikely to follow other central banks in cutting until there is greater clarity. But its policy rate of 0.75% is already well below inflation of 2%. This is close to the lowest it has ever been since the establishment of the Bank in 1694. In contrast, the European Central Bank last week hinted at lowering rates even further into negative territory.

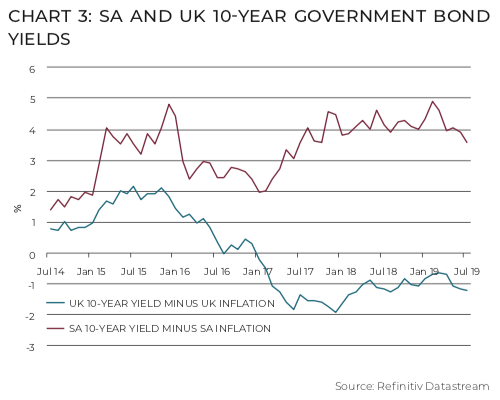

UK bond yields fell after the referendum, pricing in lower growth, with the 10-year bond yield hitting 0.55% in August 2016. (Bond yields and prices move in opposite directions.) As global bond markets rallied this year and Brexit uncertainty increased, UK yields again fell below 1%.

According to the LSL Acadata House Price Index, the average British house price rose by a respectable 4% per year in the decade to early 2018, but has declined since then as Brexit uncertainty (among other things) started biting. London house prices rose at twice the national average before the early 2018 peak, but have since fallen about 4%. Of course, the divergence in fortunes between London and the rest of the country contributed to the unhappiness that led to the Brexit vote in the first instance.

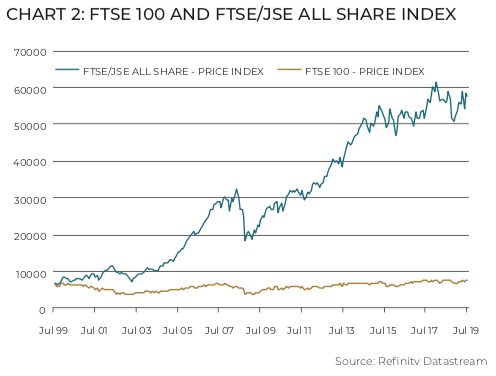

The London Stock Exchange, even more than our JSE, is dominated by companies that earn their revenues outside the UK. Specifically, it is the primary market for the world’s largest mining and resources firms. The FTSE 100 large cap index therefore benefited from post-referendum pound weakness and has returned 33% in total since then, while an index of UK government bonds delivered 14%. However, this lags the 79% return of US equities over the same period (measured in pounds). The longer-term return of UK equities is hardly exciting.

Over the past five years, the FTSE 100 delivered an annualised return of 6% in pounds, more or less the same as UK government bonds. Interestingly, the annualised sterling return of the JSE All Share over this period is also around 6%. Similarly, both indices have returned around 9% per year over the past 10 years in pound terms. The notion that South African equities have delivered a uniquely poor performance over the past decade is therefore not true. Of course, the two indices have commonalities in the dual listings of BHP, Anglo American, Old Mutual and others. But the MSCI All Countries World ex US index - which includes the UK but also the rest of Europe, Australia, Japan, China and others - also returned a 9% annualised return in pounds over this period. US equities returned 17%. When it comes to the equity markets, therefore, it was the US versus the rest over the past decade.

If we go back 20 years, the picture is very different as it included both the 2008 financial crisis and the collapse of the dotcom bubble. Over this period, UK equities delivered a 4% annual return and lags South African equities by about 6% per year (again in common currency). Twenty years ago in June 1999, the FTSE 100 Index and the JSE All Share Index had the same index value, namely 6 300 points. On Friday, the FTSE 100 closed at 7 549 points. It broke through the 6 700 points level no fewer than 13 times in the past two decades, most recently in December last year. Most of the return over this period has therefore been from dividends, not price appreciation. In contrast, the JSE All Share Index closed at 57 570 points on Friday.

Spare a thought, then, for your counterparts on the Mud Island. The last two decades have seen very little wealth creation from domestic financial markets, while the future is plagued by political uncertainty (but because they carry a large political risk premium, UK assets have become undervalued). But unlike in South Africa, interest rates are rock bottom and negative in real terms. A British investor unwilling to take equity risk does not have many other options. Although local investors have not had much to cheer about of late, we do have the benefit of high real interest rates to act as a source of income or portfolio stabilisation. Moreover, if these rates were to decline meaningfully, it would boost the prices of other assets.

RISKS PRICED IN South African assets also reflect a political risk premium. While the election has come and gone, policy uncertainty remains, as our ruling party is also divided and key decisions are not being made. The biggest millstone around South Af rican necks is Eskom. The beleaguered utility will receive a further R59 billion bailout over two years, money that will have to be borrowed by the government. Though the bailout apparently comes with strict conditions, we don’t know what these are and how enforceable they are. Moody’s, the last major ratings agency to view South Africa as investment grade, complained about this lack of clear plans to turn Eskom around in their response to the bailout announcement. Fitch responded by changing the outlook on their rating from stable to negative.

The risk of further downgrades is high, but the bond market has reflected this for a while. Foreigners have been net sellers of bonds over the past year. Although our bond yields have declined this year, this is due to global yields slumping. Other emerging market yields have fallen further and among our peers, only Turkey has higher yields. Don’t let the bailout blues (or Boris Johnson) scare you into making rash investment decisions - we have not had the worst equity market in the world over the past few years and our real interest rates are attractive.

DAVE MOHR AND IZAK ODENDAAL | OLD MUTUAL MULTI-MANAGERS

Comments